There is a lot of hype and clickbait out there on SaaS math versus AI math. And that SaaS companies are dead, and SaaS metrics are dead.

The tweet below got me thinking about SaaS economics versus AI economics. It’s a catchy take on AI versus SaaS. But is it true?

“AI companies running at 50–60% margins generate MORE absolute profit per customer. The math changed.”

As someone who spends almost everyday modeling SaaS P&Ls and calculating SaaS metrics, I decided to test the math.

Let’s find out if claim that “AI companies generate more profit per customer” holds up. The point of this post isn’t to slam or debunk this tweet, but to really get us thinking about the economics of what we are building.

You can download the Excel file used in this post below. Let’s walk through it.

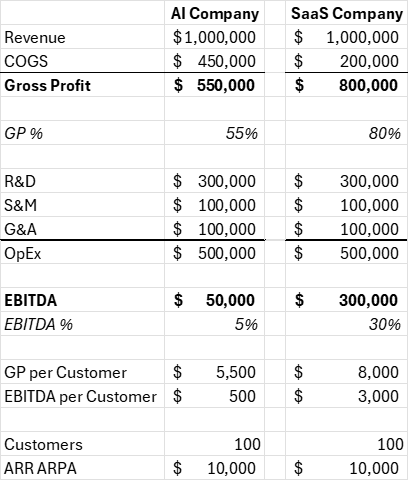

Status Quo: SaaS vs. AI at the Same Revenue and Customer Levels

Imagine a SaaS and AI company, both with $1 million in annual revenue. I’ll run with the margins mentioned in the tweet. This will be our status quo.

I picked an OpEx profile that I see a lot. Heavier R&D investment in the beginning, founder-led sales, and a light G&A profile. We’ll keep that profile the same throughout the analysis.

Here’s the comparative P&L.

The SaaS company generates $250,000 more EBITDA on the same revenue level. Of course, that makes sense because the companies have different gross profit levels.

What about the claim that AI companies “generate MORE absolute profit per customer?”

Now, I’m not sure which “profit” number they are referring to but let’s go with gross profit. The AI company cannot make more per customer because its profit margin is lower.

This assumes that both companies have the same number of customers and same ARPA. Lots of variables here, but let’s keep it easy.

The big question. How should the economics change for the AI company to look financially better from a P&L perspective?

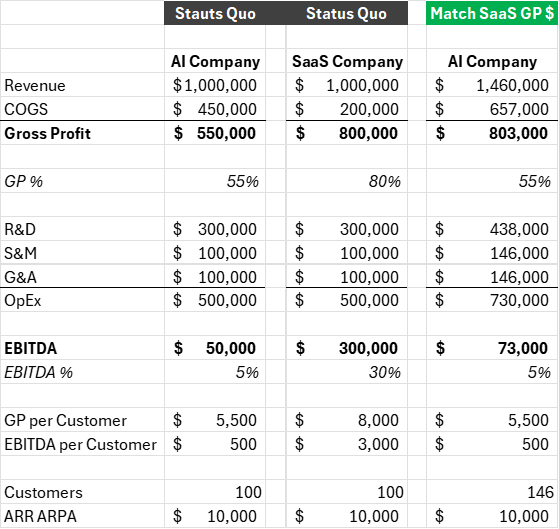

Scenario 2: AI Company Matches the SaaS Company’s Gross Profit Dollars

Let’s keep pushing on this claim that AI companies “generate MORE absolute profit per customer.” I increased the revenue of the AI company so that the absolute gross profit dollars matched the status quo SaaS company.

The AI company would need to be 46% larger from a revenue perspective to match the absolute GP dollars for the SaaS company.

Assuming no change in customer ARPA, the gross profit per customer of the AI company does not change, because the gross profit of 55% has not changed. The AI company needs more revenue to keep up with the higher SaaS gross profit percentage.

At this stage, the profit per customer is still lower and has not changed.

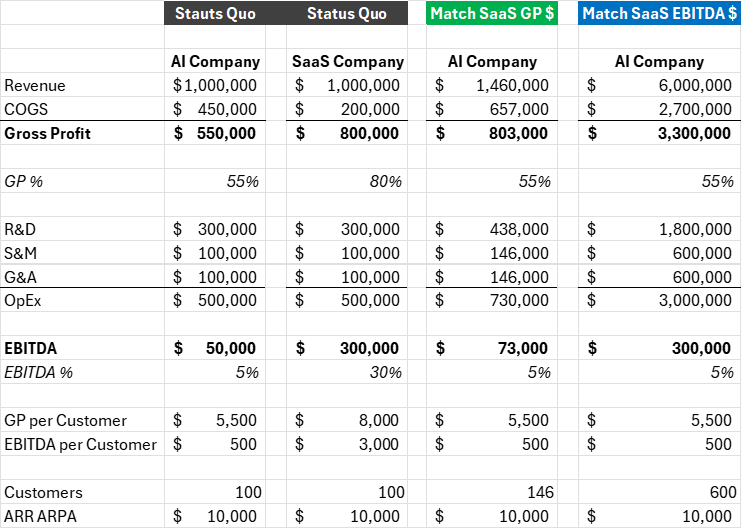

Scenario 3: AI Company Matches the SaaS Company’s EBITDA Dollars

We know private equity loves EBITDA. This long-term proxy for cash flow pays down debt and adds dollars to our bank account.

In this scenario, we want the AI company to match the EBITDA dollars produced by the SaaS company.

Bottom line. The AI company must be 6x the revenue size of the SaaS company to match the SaaS EBITDA output.

I’m holding the OpEx profile and customer ARPA constant.

The AI company is not generating more profit per customer at this stage, because I did not increase the customer ARPA.

The tweet below makes an important point. The AI software market is larger, because AI is deferring or removing people from company org charts.

We are not just fighting for the company’s software budget. We are also tapping into a much larger labor budget.

Yes, the AI company needs a larger TAM to match SaaS economics on an EBITDA-basis, but it has also proven product-market fit with a customer base of six hundred.

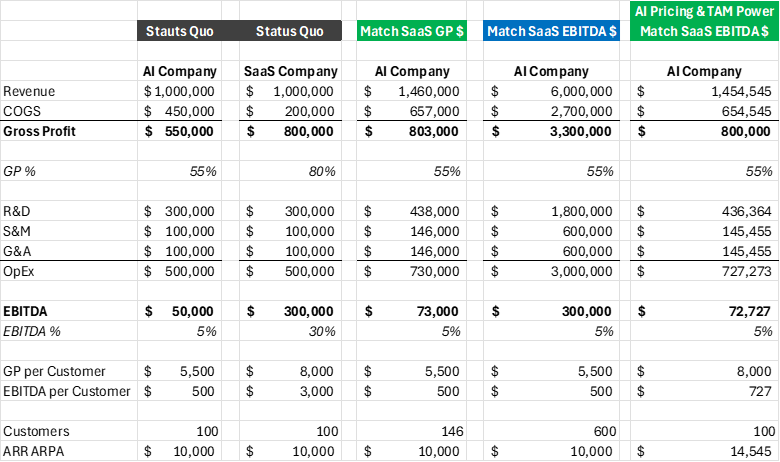

Scenario 4: AI Asserts Pricing and TAM Power

If AI companies have pricing power and a larger budget TAM, then AI should be able to assert some pricing power.

In this scenario, I adjusted the customer ARPA of the AI company so that the gross profit dollars match the SaaS company. We need a price uplift of 45% to match the SaaS profit dollars.

Same customer count but higher ARPA that takes advantage of a company’s software and labor budget.

The P&L Math Didn’t Change — the Inputs Did

The tweet says the “math changed.” It didn’t. I still assess the P&L the same way.

What did change are the cost structures and budget source to drive our revenue growth.

Traditional SaaS sells into software budgets — recurring spend, high margin, predictable scale. Once the product is built, incremental cost to produce a dollar of revenue is very low.

AI companies, on the other hand, sell into software and labor budgets. Agentic AI replaces or augments human work. That’s a bigger opportunity — but it comes with real, recurring costs: compute, inference, and model licensing.

So yes, AI may tap a 10x larger TAM, but its gross margins (40–60%) are structurally lower than SaaS (70–85%). To match SaaS profit dollars, AI has to make up for that lower delivery efficiency with higher volume and/or pricing power.

When Lower Margins Can Still Work for AI

AI’s lower margin profile doesn’t doom the model. It just changes the levers that matter most.

- Higher ARPA (Average Revenue per Account): If your AI product replaces $200K of labor, you may be able to $100K per customer instead of $20K for SaaS.

- Larger TAM: AI addresses a bigger spend category. If your total market is 10x larger, even lower margins can scale to bigger profit pools.

- Falling compute costs: Over time, inference costs may drop — improving margin without changing price. There is a lot of debate on this.

- Retention is front and center. With lower margins, the path to profitability will require acute focus on gross revenue retention and net revenue retention.

- CAC Payback what? Another huge use of cash in your business is the go-to-market machine. If you didn’t go viral like Cursor, Lovable, or Replit, you’ll need to monitor your GTM efficiency metrics.

But until those things happen, comparing AI and SaaS profit dollars at equal revenue is misleading without the proper context above.

The Great Value Unlock – Higher Gross Profit Margin

I see this a lot in SaaS. Low gross profit in the 50-60% range is a big hurdle. If you are bootstrapped with lower cash balances, it’s very difficult to invest and scale rapidly.

Why is this different for AI? The rapid scale and bigger TAM. It’s still up for debate on where AI gross profit margins will trend.

Some AI companies produce SaaS-like margins and print money. Others, with lower margins, need a lot of scale to match their SaaS colleagues.

Implications for Founders and CFOs

If you’re building an AI company or investing in AI businesses, here’s what to keep in mind:

- Gross margin still matters. Even if compute costs are “normal” for AI, the business still needs margin expansion to scale profitably or a huge TAM.

- Track the fundamentals. Build your P&L to see gross profit and margins by revenue stream. Track your OpEx profile, EBITDA, CAC Payback Period, retention, and ARPA.

- Model your TAM × Margin. Lower margins are fine if the market is big enough. Your unit economics need to justify that trade-off.

- Valuations impact. The SaaS “Rule of 40” is all about the balance between profit and growth. But AI companies are attracting high valuations and capital due to their massive growth profile. What happens if that company cannot produce decent EBITDA margins? Eventually, you need positive cash flow whether you call yourself AI, SaaS, or software.

AI companies can absolutely build profitable, durable businesses — but the path looks different. Not everyone will be an AI unicorn. The metrics and math aren’t broken; the economics are just new.

The Takeaways

The “AI vs. SaaS” debate isn’t about which model is better. It’s about understanding why the numbers look different.

If SaaS is about margin efficiency, AI is about value density — how much output, productivity, or labor you replace per dollar of cost.

So the next time you see a post claiming “AI companies make more profit per customer,” remember:

- Profit per customer only beats SaaS if the average revenue per customer is meaningfully higher.

- The math didn’t change. The inputs did — and that’s where operators should focus.

Download my Excel template used in this post below.

I have worked in finance and accounting for 25+ years. I’ve been a SaaS CFO for 9+ years and began my career in the FP&A function. I hold an active Tennessee CPA license and earned my undergraduate degree from the University of Colorado at Boulder and MBA from the University of Iowa. I offer coaching, fractional CFO services, and SaaS finance courses.

Love this analysis. The one version I was looking to see, that I didn’t, was a different OPEX profile. A lot of these AI companies tout how low of a headcount base they have, ~50-100 people on $100M+ in ARR. So my expectation is their opex profiles may be significantly lower than what you’d see in a traditional SaaS company. Is there any truth to that?

Hi Alex, yes, you do hear about those cases where the generate 1M per FTE. But it seems like they would have an internal effort to do as much as possible with AI. Not sure if that’s the case for all AI companies.

Hi Ben, I do not understand well. My impression is that SaaS is dead because AI is replacing it. The key question in my view is the actual fundamental value drivers of SaaS versus AI. Not sure why AI generally have lower gross profit margin, nor why ARPA would be higher for AI then SaaS. My basic question is when looking at SaaS propositions is whether they are at all defendable with the upcoming AI disruption. I cannot get a clear answer. happy to have a more in depth discussion my email is [email protected]. Best, Andrei

Hi Andrei, the verdict is still out on AI Margins but I think they will eventually be like SaaS margins.